用IT技术玩金融系列文章,将介绍如何使用IT技术,处理金融大数据。在互联网混迹多年,已经熟练掌握一些IT技术。单纯地在互联网做开发,总觉得使劲的方式不对。要想靠技术养活自己,就要把技术变现。通过“跨界”可以寻找新的机会,创造技术的壁垒。

金融是离钱最近的市场,也是变现的好渠道!今天就开始踏上“用IT技术玩金融”之旅!

关于作者:

- 张丹(Conan), 程序员Java,R,PHP,Javascript

- weibo:@Conan_Z

- blog: http://blog.fens.me

- email: bsspirit@gmail.com

转载请注明出处:

http://blog.fens.me/finance-rhive-repurchase/

前言

接触金融时间并不太长,对我来说第一个操作的业务,就是逆回购。逆回购对于大部分人来说,都是一个新鲜词,就算是炒股多年的玩家,可能也是在2013年6月份发生银行缺钱的事件之后才了解的。隔夜的银行间拆借利率达到了30%,简单来说银行缺钱了!各种机构 分分出售股票,债券,兑换成现金借给应银行。个人用户也都取出存款,通过逆回购,把钱借给银行。30%的利率,让所有人在那一周都为之兴奋,只有银行在惶恐。

目录

- 逆回购简介

- 历史数据模型

- 通过用RHive提取数据

- 简单策略实现

1. 逆回购简介

债券回购的含义

债券质押式回购简单地说就是交易双方以债券为质押品的一种短期资金借贷行为。其中债券持有人(正回购方)将债券质押而获得资金使用权,到约定的时间还本并支付一定的利息,从而“赎回”债券。而资金持有人(逆回购方)就是正回购方的交易对手。在实际交易中债券是质押给了第三方即中国结算公司,这样交易双方否更加安全、便捷。

可回购的债券

所有的国债、绝大部分企业债、公司债和分离债的纯债都可用于债券回购交易。沪深交易所每周都会公布可回购债券的折算率,上面没有但可交易的品种就是不可回购的债券。折算率简单说,就是把债券质押时,交易所按债券面值给出的可质押的比率。

现在交易的回购品种

我们仅列出个人投资者经常参与的公司债(包括企业债等)回购品种。

上海证券交易所可交易的质押式回购(括弧中为交易代码)分为1日(204001)、2日(204002)、3日(204003)、4日(204004)、7日(204007)、14日(204014)、28日(204028)、91日(204091)、182日(204182)共9个品种。深圳交易所按回购期限分为分为1日(131810)、2日(131811)、3日(131800)、7日(131801)共4个品种。其中经常交易的只有沪深1日和7日四个品种,并且沪市的日均交易量又远远大于深市的交易量。

以上逆回购定义摘自:http://finance.sina.com.cn/money/bond/20121016/180713385513.shtml

2. 历史数据模型

Hive中的表结构:

rhive.desc.table('t_reverse_repurchase')

col_name data_type

1 tradedate string

2 tradetime string

3 securityid string

4 bidpx1 double

5 bidsize1 double

6 offerpx1 double

7 offersize1 double

tradedate:交易日期

tradetime:交易时间

securityid:股票ID

bidpx1:买一

bidsize1:买一交易量

offerpx1:卖一

bidsize1:卖一交易量

3. 通过用RHive提取数据

登陆c1服务器,打开R的客户端。

#装载RHive

library(RHive)

#初始化

rhive.init()

#连接到Hive集群

> rhive.connect("c1.wtmart.com")

SLF4J: Class path contains multiple SLF4J bindings.

SLF4J: Found binding in [jar:file:/home/cos/toolkit/hive-0.9.0/lib/slf4j-log4j12-1.6.1.jar!/org/slf4j/impl/StaticLoggerBinder.class]

SLF4J: Found binding in [jar:file:/home/cos/toolkit/hadoop-1.0.3/lib/slf4j-log4j12-1.4.3.jar!/org/slf4j/impl/StaticLoggerBinder.class]

SLF4J: See http://www.slf4j.org/codes.html#multiple_bindings for an explanation.

#查看当前的表

> rhive.list.tables()

tab_name

1 t_hft_day //历史数据表

2 t_hft_tmp //临时表

4 t_reverse_repurchase //逆回购表

查看所有股票历史数据分片:测试数据从20130627–20130726。

> rhive.query("SHOW PARTITIONS t_hft_day");

partition

1 tradedate=20130627

2 tradedate=20130628

3 tradedate=20130701

4 tradedate=20130702

5 tradedate=20130703

6 tradedate=20130704

7 tradedate=20130705

8 tradedate=20130708

9 tradedate=20130709

10 tradedate=20130710

11 tradedate=20130712

12 tradedate=20130715

13 tradedate=20130716

14 tradedate=20130719

15 tradedate=20130722

16 tradedate=20130723

17 tradedate=20130724

18 tradedate=20130725

19 tradedate=20130726

分为提取”上交所一天逆回购”(204001),和”深交所一天逆回购”(131810),从7月22日至7月26日的一周数据。

> rhive.drop.table("t_reverse_repurchase")

> rhive.query("CREATE TABLE t_reverse_repurchase AS SELECT tradedate,tradetime,securityid,bidpx1,bidsize1,offerpx1,offersize1 FROM t_hft_day where tradedate>=20130722 and tradedate<=20130726 and securityid in (131810,204001)");

查看数据结果集

> rhive.query("SELECT securityid,count(1) FROM t_reverse_repurchase group by securityid");

securityid X_c1

1 131810 17061

2 204001 12441

加载到R的内存中。

> bidpx1<-rhive.query("SELECT securityid,concat(tradedate,tradetime) as tradetime,bidpx1 FROM t_reverse_repurchase");

#查看记录条数

> nrow(bidpx1)

[1] 29502

#查看数据

> head(bidpx1)

securityid tradetime bidpx1

1 131810 20130724145004 2.620

2 131810 20130724145101 2.860

3 131810 20130724145128 2.850

4 131810 20130724145143 2.603

5 131810 20130724144831 2.890

6 131810 20130724145222 2.600

用ggplot2做数据可视化

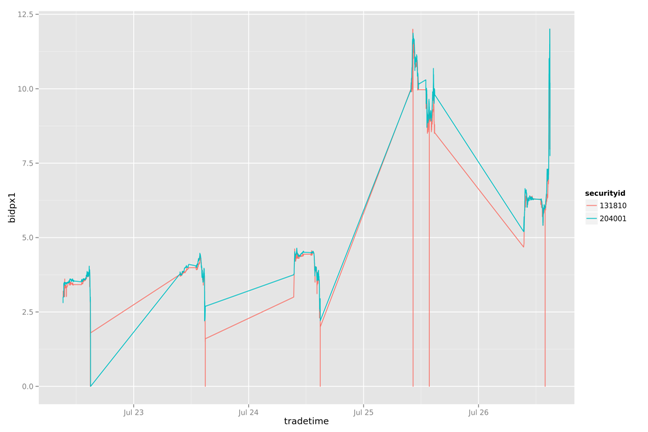

一周数据的走势

library(ggplot2)

g<-ggplot(data=bidpx1, aes(x=as.POSIXct(tradetime,format="%Y%m%d%H%M%S"), y=bidpx1))

g<-g+geom_line(aes(group=securityid,colour=securityid))

g<-g+xlab('tradetime')+ylab('bidpx1')

ggsave(g,file="01.png",width=12,height=8)

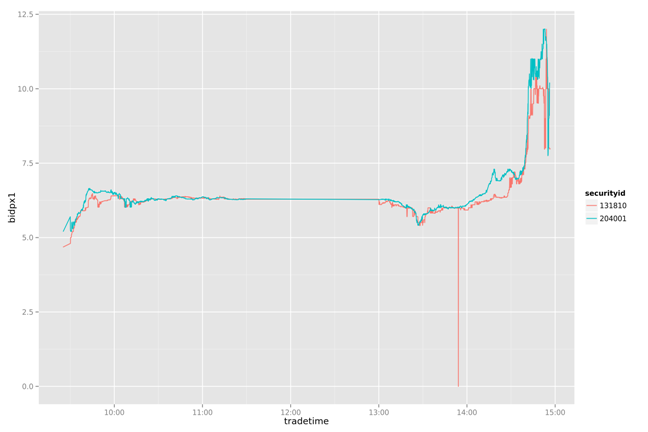

一天数据的走势

bidpx1<-rhive.query("SELECT securityid,concat(tradedate,tradetime) as tradetime,bidpx1 FROM t_reverse_repurchase WHERE tradedate=20130726");

g<-ggplot(data=bidpx1, aes(x=as.POSIXct(tradetime,format="%Y%m%d%H%M%S"), y=bidpx1))

g<-g+geom_line(aes(group=securityid,colour=securityid))

g<-g+xlab('tradetime')+ylab('bidpx1')

ggsave(g,file="02.png",width=12,height=8)

4. 简单策略实现

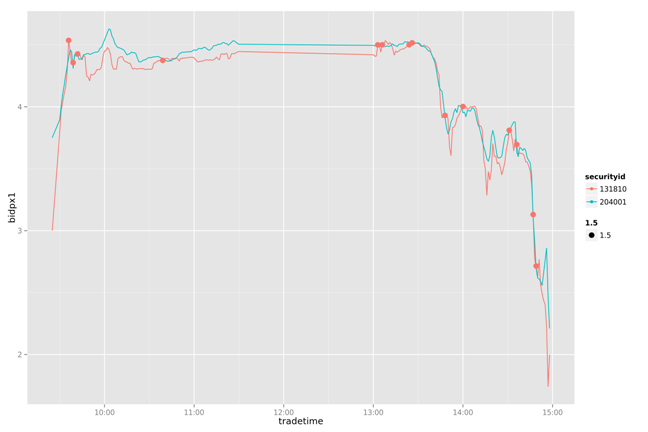

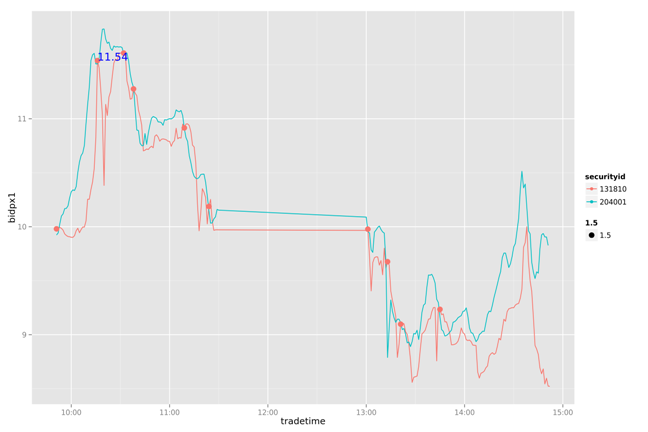

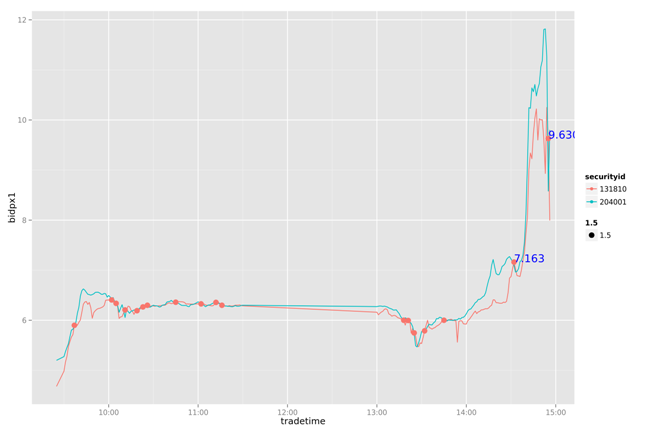

通过简单的打印出两幅图片的两条曲线,我们可以看到131810一直在追随204001变化,并且大部情况都低于204001。

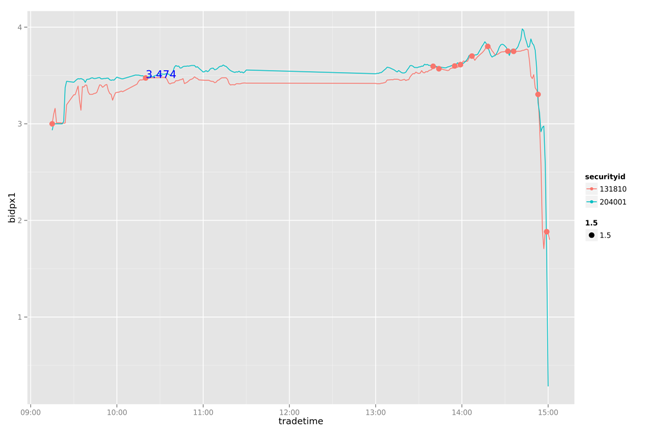

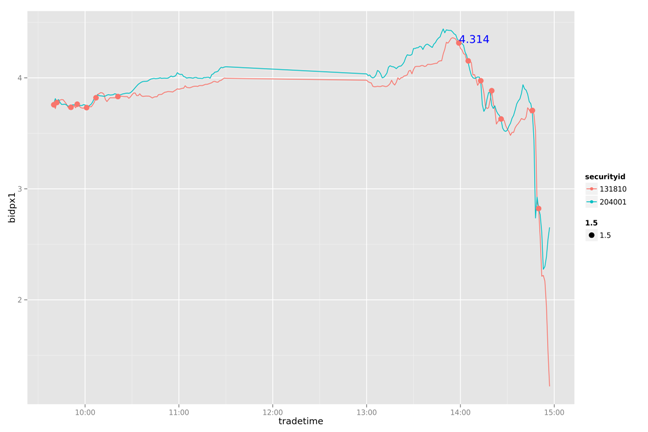

下面做一个简单的策略分析:通过204001变化,判断131810的卖点。

- 把131810和204001按每分钟标准化

- 设置当131810和204001有交点的时候,提取卖出信号

- 当后一个交点的卖一价格大于前一个交点的卖一价格10%以上,做为局部最优的卖出信号点

提取131810,204001的数据,存储在t_reverse_repurchase表中

#登陆R

library(RHive)

rhive.init()

rhive.connect("c1.wtmart.com")

#提取131810,204001的数据

rhive.drop.table("t_reverse_repurchase")

rhive.query("CREATE TABLE t_reverse_repurchase AS SELECT tradedate,tradetime,securityid,bidpx1,bidsize1,offerpx1,offersize1 FROM t_hft_day where securityid in (131810,204001)");

#查看数据集

rhive.query("select count(1),tradedate from t_reverse_repurchase group by tradedate")

X_c0 tradedate

1 4840 20130627

2 4792 20130628

3 4677 20130701

4 3124 20130702

5 2328 20130703

6 3787 20130704

7 4294 20130705

8 4977 20130708

9 4568 20130709

10 6619 20130710

11 5633 20130712

12 6159 20130715

13 5918 20130716

14 6200 20130719

15 6074 20130722

16 5991 20130723

17 5899 20130724

18 5346 20130725

19 6192 20130726

加载软件包

library(ggplot2)

library(scales)

library(plyr)

获得一天的数据并做ETL

#把一周的数据加载到内存

bidpx1<-rhive.query(paste("SELECT securityid,tradedate,tradetime,bidpx1 FROM t_reverse_repurchase WHERE tradedate>=20130722"));

#加载一天的数据并做ETL

oneDay<-function(date){

d1<-bidpx1[which(bidpx1$tradedate==date),]

d1$tradetime2<-round( as.numeric(as.character(d1$tradetime))/100)*100

d1$tradetime2[which(d1$tradetime2<100000)]<-paste(0,d1$tradetime2[which(d1$tradetime2<100000)],sep="")

d1$tradetime2[which(d1$tradetime2=='1e+05')]='100000'

d1$tradetime2[which(d1$tradetime2=='096000')]='100000'

d1$tradetime2[which(d1$tradetime2=='106000')]='110000'

d1$tradetime2[which(d1$tradetime2=='126000')]='130000'

d1$tradetime2[which(d1$tradetime2=='136000')]='140000'

d1$tradetime2[which(d1$tradetime2=='146000')]='150000'

d1

}

#通过均值标准化

meanScale<-function(d1){

ddply(d1, .(securityid,tradetime2), summarize, bidpx1=mean(bidpx1))

}

#找到要分析的点

findPoint<-function(a1,a2){

#找到所有a1大于a2的点

bigger_point<-function(a1,a2){

idx<-c()

for(i in intersect(a1$tradetime2,a2$tradetime2)){

i1<-which(a1$tradetime2==i)

i2<-which(a2$tradetime2==i)

if(a1$bidpx1[i1]-a2$bidpx1[i2]>=-0.02){

idx<-c(idx,i1)

}

}

idx

}

#去掉连续的索引值

remove_continuous_point<-function(idx){

idx[-which(idx-c(NA,rev(rev(idx)[-1]))==1)]

}

idx<-bigger_point(a1,a2)

remove_continuous_point(idx)

}

#发现局部最优卖出点

findOptimize<-function(d3){

idx2<-which((d3$bidpx1-c(NA,rev(rev(d3$bidpx1)[-1])))/d3$bidpx1>0.1)

if(length(idx2)<1)

print("No Optimize point")

d3[idx2,]

}

#画图查看结果

draw<-function(d2,d3,d4,date,png=FALSE){

g<-ggplot(data=d2, aes(x=strptime(paste(date,tradetime2,sep=""),format="%Y%m%d%H%M%S"), y=bidpx1))

g<-g+geom_line(aes(group=securityid,colour=securityid))

g<-g+geom_point(data=d3,aes(size=1.5,colour=securityid)) if(nrow(d4)>0){

g<-g+geom_text(data=d4,aes(label= format(d4$bidpx1,digits=4)),colour="blue",hjust=0, vjust=0)

}

g<-g+xlab('tradetime')+ylab('bidpx1')

if(png){

ggsave(g,file=paste(date,".png",sep=""),width=12,height=8)

}else{

g

}

}

#执行策略封装

date<-20130722

d1<-oneDay(date)

d2<-meanScale(d1)

a1<-d2[which(d2$securityid==131810),]

a2<-d2[which(d2$securityid==204001),]

d3<-d2[findPoint(a1,a2),]

d4<-findOptimize(d3)

draw(d2,d3,d4,as.character(date),TRUE)

20130722

20130723

20130724

20130725

20130726

通过对一周数据的比较我们发现,这个简单的策略能我们带来一些收益。虽然不是全局最优的,但比人为的判断会更有依据。

用IT技术玩金融系列文章,第一篇就当是一个抛砖引玉的开始,后面的文章会更精彩。

######################################################

看文字不过瘾,作者视频讲解,请访问网站:http://onbook.me/video

######################################################

转载请注明出处:

http://blog.fens.me/finance-rhive-repurchase/